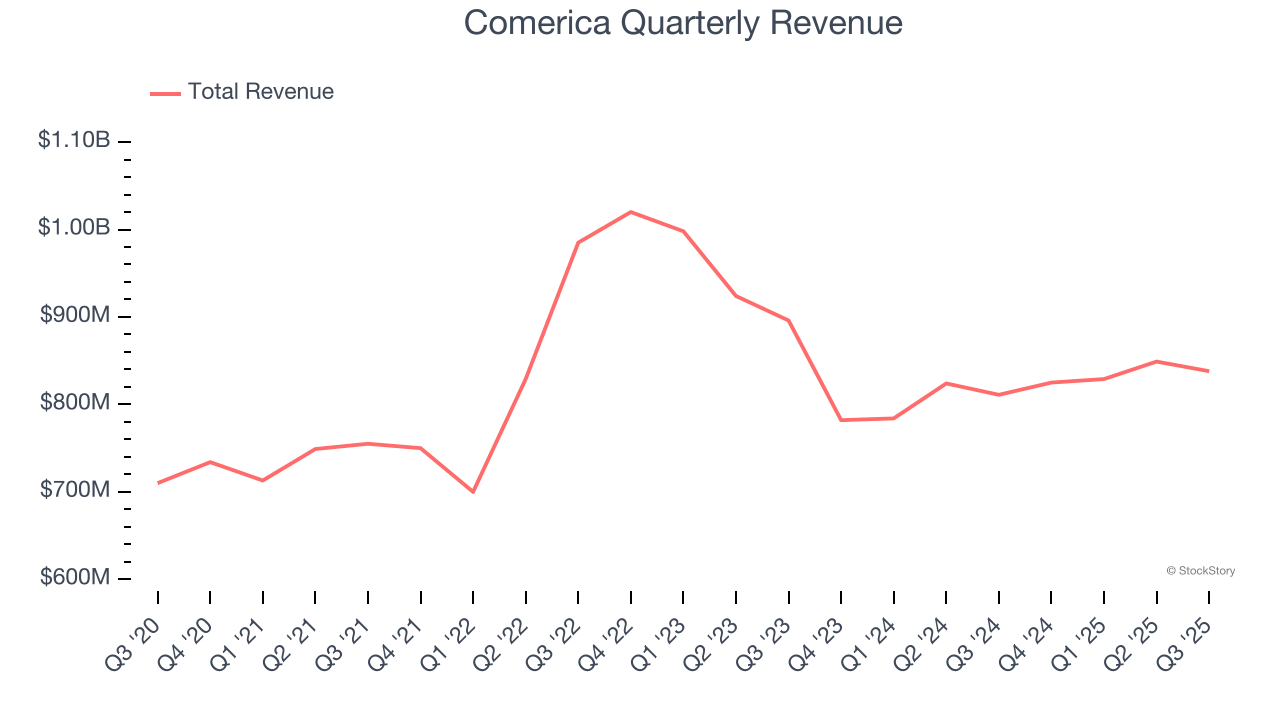

Financial services company Comerica (NYSE:CMA) missed Wall Street’s revenue expectations in Q3 CY2025 as sales rose 3.3% year on year to $838 million. Its GAAP profit of $1.35 per share was 3.4% above analysts’ consensus estimates.

Is now the time to buy Comerica? Find out by accessing our full research report, it’s free for active Edge members.

Comerica (CMA) Q3 CY2025 Highlights:

- Net Interest Income: $574 million vs analyst estimates of $569.1 million (7.5% year-on-year growth, 0.9% beat)

- Net Interest Margin: 3.1% vs analyst estimates of 3.2% (6.2 basis point miss)

- Revenue: $838 million vs analyst estimates of $842.6 million (3.3% year-on-year growth, 0.6% miss)

- Efficiency Ratio: 70.2% vs analyst estimates of 70.8% (55.4 basis point beat)

- EPS (GAAP): $1.35 vs analyst estimates of $1.31 (3.4% beat)

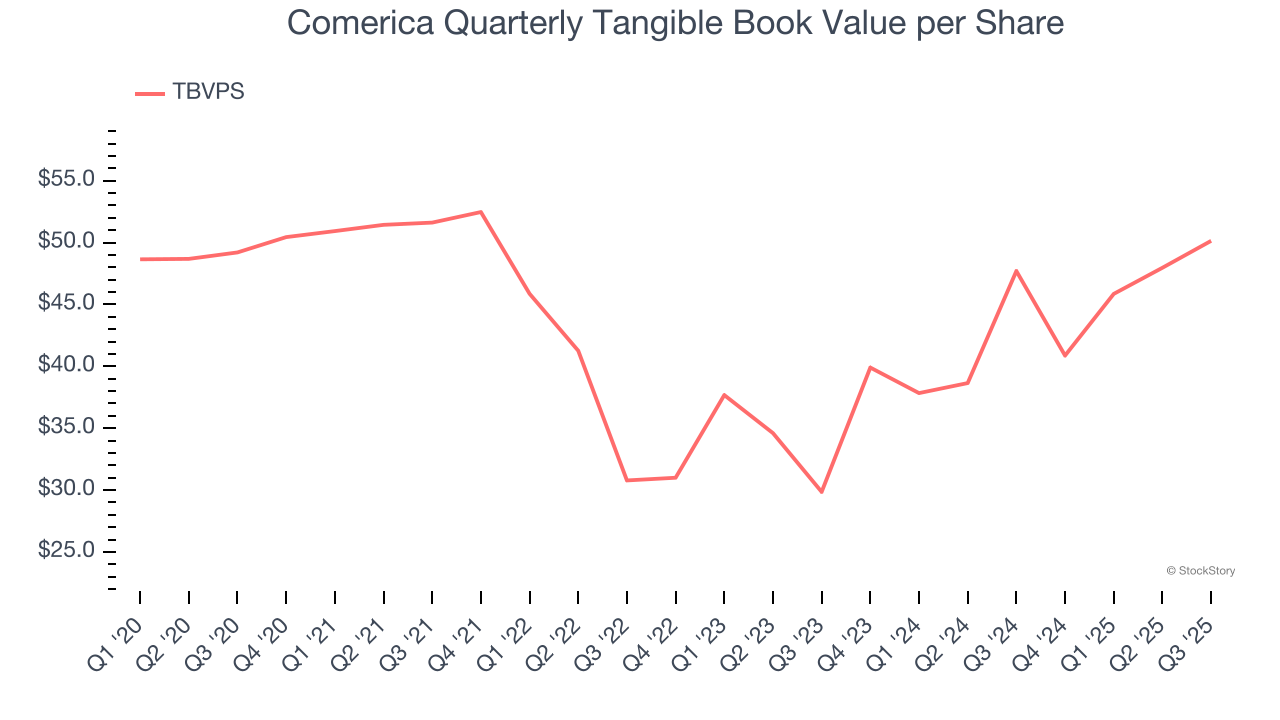

- Tangible Book Value per Share: $50.14 vs analyst estimates of $48.12 (5.1% year-on-year growth, 4.2% beat)

- Market Capitalization: $9.49 billion

Company Overview

Founded in 1849 during the California Gold Rush era, Comerica (NYSE:CMA) is a financial services company that provides commercial banking, retail banking, and wealth management services to businesses and individuals.

Sales Growth

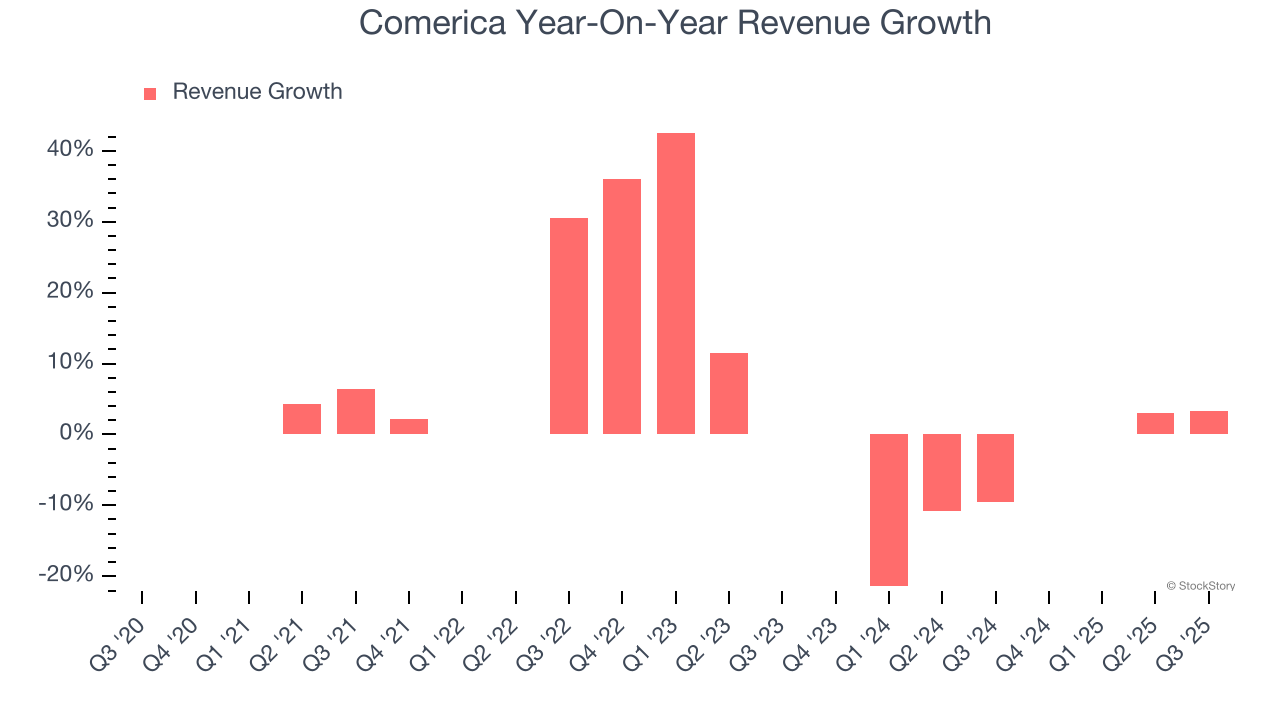

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income. Over the last five years, Comerica grew its revenue at a tepid 2.3% compounded annual growth rate. This was below our standards and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Comerica’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.7% annually.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Comerica’s revenue grew by 3.3% year on year to $838 million, falling short of Wall Street’s estimates.

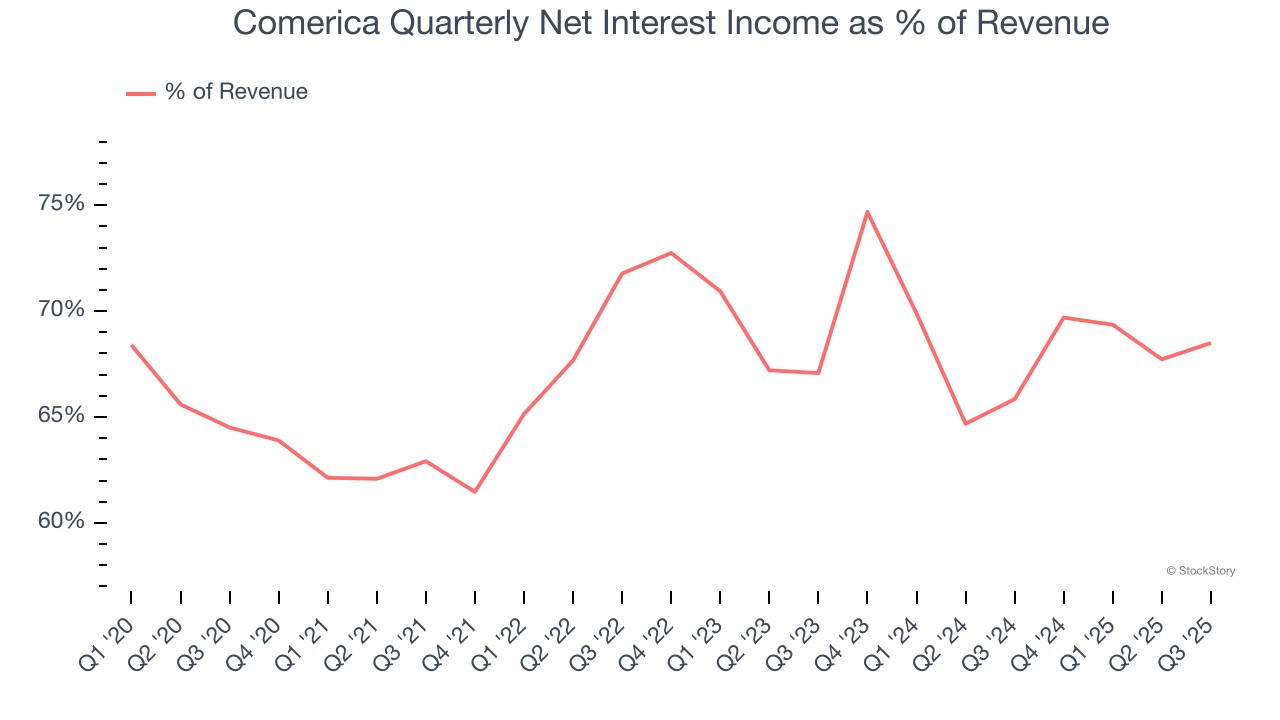

Net interest income made up 67.3% of the company’s total revenue during the last five years, meaning lending operations are Comerica’s largest source of revenue.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

Comerica’s TBVPS was flat over the last five years. However, TBVPS growth has accelerated recently, growing by 29.6% annually over the last two years from $29.86 to $50.14 per share.

Over the next 12 months, Consensus estimates call for Comerica’s TBVPS to grow by 2.8% to $51.55, paltry growth rate.

Key Takeaways from Comerica’s Q3 Results

We enjoyed seeing Comerica beat analysts’ tangible book value per share expectations this quarter. We were also happy its net interest income narrowly outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed and its EPS slightly exceeded Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $73.26 immediately following the results.

So do we think Comerica is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.